John Dougall: Keeping Honest People Honest

Unlocking Utah Politics with Stan Lockhart: Episode 8

I had the opportunity to sit down with John Dougall to talk about his role as Utah State Auditor. A large part of his responsibility is ensuring that government entities are using funds responsibly: “A big part of my job is to make sure that government is accountable to the public, I’m helping the public in their oversight responsibilities.”

Good People Who Make Bad Choices

A large part of John’s job is dealing with fraud charges. John Dougall talked about how often there is the misconception that people who commit fraud are bad people:

“I have people talk to me, you must deal with a lot of bad people, and I tell them that I typically deal with a lot of good people that made bad choices. With a certain type of opportunity, with certain pressure, any one of us can start rationalizing certain behavior that we would never engage in normally, but we’re stuck in a difficult situation. And so, part of auditing is trying to help keep honest people honest.”

John Dougall gave the example of when you lock your door to your car or to your house: “If somebody really wants to get in they can get in. But for a lot of folks they’ll check that door knob, that door handle, and if it’s locked they’ll keep going. And that’s part of what auditing is, it’s helping keep honest people honest.”

That is the way that fraud works. John said, “The assumption is the auditors aren’t going to check, management isn’t going to check, certain folks will start cutting corners. But if the belief is somebody’s going to check up then most folks are going to be conscientious and do their job. But we have to recognize that we all have weaknesses, we’re all human and we can all succumb to certain pressures.”

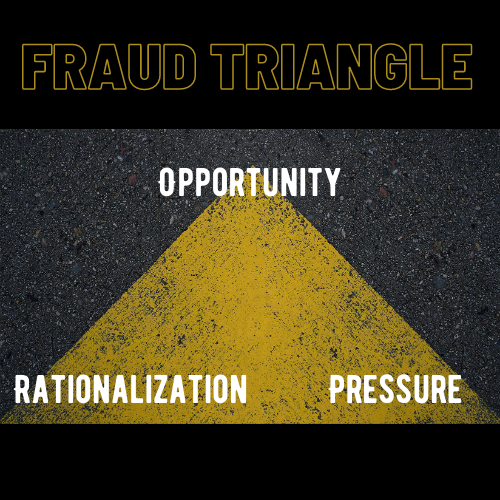

Fraud Triangle:

John Dougall talked about a concept that they have found helpful in identifying fraud. They call it the fraud triangle. When opportunity, pressure, and rationalization come together, there’s a heightened risk of fraud and stuff.

An example of the fraud triangle is the case of a county official stealing funds. This case had all the sides of the fraud triangle.

Opportunity: There was opportunity clearly. The treasurer deals with the money so there is the opportunity to take money.

Pressure: There was pressure, historically there had been financial pressures in the family. When they were investigating and talking to the sheriff, he said he knew where she lived because he’d served a foreclosure notice there for her home. So, there’s financial pressures there.

Rationalization: They later learned that her county credit card had been taken away for misuse.

And so, you know, there’s opportunity, there’s pressure, and then when somebody starts to rationalize why it’s okay to take public funds,

John Dougall said, “All those type of things together create a heightened risk of fraud. It doesn’t mean that there is fraud, but it just means you need to watch for it. And so, we tell government officials that the opportunities are where you can usually control it the best, you typically don’t know people’s pressure, you don’t know their rationalization, but you do know the opportunity and you can separate duties and other things like that when it comes to opportunity to try and reduce the risk of fraud.”

Fraud Examples:

$190K to Board Chair:

When John had been in office about 14 months he issued a press release about offices that were delinquent in their payments. One of the offices mentioned came out and told the press that his office didn’t have their fax machine on because if they did they would get their reports.

As soon as they started investigating, they found out that the office had just written checks to board members that ended up draining half their bank accounts. The board chair got $190,000 and the vice chair got $80,000. According to state law, they can’t receive more than $5,000 a year.

John said, “So Stan, even you that’s not a math guy, knows the difference between 190 thousand and five thousand, okay. What had happened is they had largely volunteered, they had never been paid and all of a sudden they woke up, the board chair was planning to retire and they wanted to give him a little, if you will, going away gift.”

The State Auditor office came in and told them the payments were illegal and recovered the money. John said, “And so, that’s one of those key things. Partly it’s holding that district accountable, but partly it’s sending a message to others.”

Irrigation District: Fake Credit Card Statements

Another example was an irrigation district in Southern Utah County.

The board just trusted their financial director and let her take care of all the money. She made all the deposits and everything else like that.

Then the State Auditor office saw some inconsistencies, they had been delinquent in some reports, so they had subpoenaed their bank records, and saw some expenditures that were questionable like payments to Chase bank for a credit card when the district didn’t have any credit card.

John Dougall said, “Now, my team met with the board chair and the water master, they said, ‘No. No, you guys are wrong. She’s wonderful.’ And when we met with her and she quickly confessed that she was taking money. She was taking extra payments to her business, to herself personally, and paying her credit card.”

She went home and added up all the charges and came up with a total of a little over $103,000. She plead guilty and they were able to recover the money.

John said, “You need them to know you can’t just turn over responsibilities without any oversight. I mean yes, you put people in those positions because you trust them, but as Reagan said, ‘Trust but verify.’ It’s the duty of those board members to verify what’s going on. And we’ve seen other dynamics like that.”

Secretary Taking $1 Million

Another organization had an audit and they found evidence of fraud for the past 10 years. After an investigation, they found that the secretary had stolen over $1,000,000 from the organization.

John Dougall said, “She was creating bogus credit card statements. She had actually printed the legitimate one on the printer and forgot to pick it up. And the credit card statement made its way to the chief financial officer who looked at it and didn’t know what it was. Then he figured out this was a real credit card statement versus the ones he had seen for the last ten years, which were all bogus.”

Projects:

The Utah State Auditor’s Office is involved in many projects to ensure that Utah taxpayers’ money is being spent responsibly.

Project Kids: Where Money Goes in Education

One of the projects that the State Auditor’s office is working on is Project Kids. They want to figure out exactly where the money in public education goes so that the stakeholders can determine how well is it really being spent.

John Dougall shared a story about the issues determining education spending:

“So, historically when I go talk with a superintendent, whether it’s the state superintendent or a local one, if I ask how much do you spend on teacher pay within a couple minutes they can pull the report and they can tell me.”

“If I ask how much do you spend on math instruction, pretty much nobody can answer. If I say how much are we spending on science instruction relative to the outcomes that we’re getting, statewide testing, in classroom assessments, whatever it might be, most folks don’t look at it that way.”

“And so we have been drilling down to the student level, what is the average cost on a student by student basis and then rolling that up. So, we can see what does it cost per class, per course, per curricular topic, other things like that. And so we can now see what is the real cost of Mr. Smith’s science class versus Mrs. Jones’ science class. And we can take dollars relative to outcomes, whether it’s GPA, in class tests, district assessments, state testing, and all that type of stuff and you can start seeing dollars versus outcome.”

“And so we’re hoping that this will better help stakeholders see where the money was going. We’re not trying to say green good or red bad, we’re just saying here’s what happened, now you determine if that’s the case. And so it’s an interesting thing which oftentimes when money is flowing based on formula you assume you’re getting certain outcomes but you don’t necessarily know what’s happening and where the money really went. So, we’re pretty excited about that project.”

Health Cost Tool

Another project that Auditor’s Office is working on developing is a health cost analysis tool.

John said, “We’re all concerned about the cost of health care. Typically when we go in we don’t know what procedures cost and so a couple months ago we launched a new website, healthcost.utah.gov.”

“And if you got to healthcost.utah.gov you can look for over 100 procedures, stand-alone procedures and see what the cost is. So urinalysis, at one lab it may be four dollars, but at the hospital it may be 40. It’s the same test, but you’re spending ten times as much at one location versus another.”

They are working on adding more procedures into the database so people can look at the costs. The goal is to help people understand the average cost per provider for health procedures across the state, and we hope that will really help improve and contain the cost of healthcare. Which we all know is just growing disproportionately and taxpayers can’t fund it, the public is struggling to pay for it, and so we hope that helps here in Utah.

Cost Does Not Equal Quality for Healthcare

I shared my experience with my son who has been shopping around to doctors trying to figure out the best cost for a procedure. The procedure is anywhere between $1,500 and $2,100 depending on the provider. And then you have to start saying well does that mean that one provider is less competent than another provider, and there’s no way to judge that.

So literally you just kind of have to say okay based on everything we know about a provider is this cost the cost we want to pay, and I think we’ve kind of gotten away from the lowest cost because we just don’t know what that means, but somewhere in the middle is where we’re going to land on getting that procedure done.

John Dougall made the point that cost does not always equal quality: “Well we oftentimes in the private sector think more expensive is a higher quality, so it’s better. But that’s not the case in healthcare. Cost and quality are disconnected in most things. However, not when it comes to healthcare, and we don’t necessarily understand that.”

State Auditor Responsibilities

Not many people are aware of what the state auditor’s roles and responsibilities are. I asked John to explain what the State Auditor does.

Financial Statement Audits

“So, one of the key things, the bread and butter historically for the office is to do the financial statement audits for the state and public colleges and universities. And each of those entities has an incentive to perhaps make themselves look better than they really are. And so we come in, we review their financial statements, and we issue an opinion whether or not they fairly represent the financial position of that organization.”

Local Government:

“We also oversee the local governments. So, there’s about about 1,000 cities and counties, and school districts, and special and local districts, transit districts, cemetery districts, water districts, irrigation districts, and so forth. And we make sure they properly adopt their budgets, we make sure they submit their end of year financial reports. We train the CPA firms that audit many of those large organizations, and it’s just trying to hold them accountable.”

“And I believe it’s important that they properly submit their budgets because it informs the public how they intend to spend the public’s money, and it’s important that they submit timely end of year reports because it tells the public how they actually spent the public’s money.”

Special Projects:

“We also have an investigative group called special projects. So, when it deals with waste, fraud, and abuse. When you hear about a financial officer stealing money typically that’s the team investigating that issue. Then we turn it over to either the county attorneys or the attorney general’s office for possible criminal prosecution.”

Audit Teams:

“We have an IT audit team because the state and local governments have pretty complex data systems and oftentimes has very sensitive data in there and so we review the controls over those systems.”

“And then we have a performance audit team that looks to see how well government’s operating, how well are they complying with the regulations, and how effective the various government programs are.”

“And then we have a data team that does a lot of big data analysis and stuff to look at where the money’s going. We currently run the financial transparency website, we call it Transparent Utah. You can go to transparent.utah.gov to access it. It basically opens the check register for the state and all local governmental. That’s kind of what we do in a nutshell.”

State Auditor is Member of Executive Branch

The state auditor is an elected position, so it’s a four year term. So, it’s elected on the same cycle as the governor, and the attorney general, and the state treasurer. The auditor is a Constitutional office in the executive branch.

Executive Branch

And when we talk about the executive branch we’re so trained in school to think about the federal level, which you have the president, the sole executive. But in Utah we actually have several executives, we have the governor, we have the lieutenant governor, we have the attorney general, the auditor, and the treasurer. We also have the state board of education, which I think is technically part of the executive branch.

So, we have checks and balances all within the executive branch, which is kind of a foreign concept that we don’t really learn about.

Lessons Learned with John Dougall:

- John’s style is transparent: He wants the expectations to be clear. If he can warn people and give them hints and direction before the end of the audit he wants to do that so they can make changes and already be better by the time that’s over.

- The auditor is within the executive branch: He is a check and balance within that branch of government. Normally, we think of checks and balances being legislative and executive and judicial branches putting checks on each other. John is in the executive branch. He holds government agencies accountable.

- Fraud Triangle: It is when opportunity, pressure, and rationalization meet.

- The auditor keeps honest people honest.